- “To no one’s surprise, Hungary’s coronavirus emergency bill — which criminalizes fake news — has already resulted in police detaining and questioning social media users who criticize Orbán.” [Sarah McLaughlin] “Part of the powers granted to the government by the coronavirus authorization act is the ability to criminally prosecute the spreading of false news which inhibits the ability of authorities to defend against the pandemic. András recalled that the police arrived at his home at 6 a.m. with a search warrant.” [Insight Hungary 444]

- The more you know about past abuses under the former FCC public interest standard, the less sanguine you will be about inviting the government to regulate the fairness of social media platforms [John Samples and Paul Matzko]

- “China-Style Internet Control Is One of the Worst Ideas for Solving Coronavirus” [Ilya Shapiro] “China’s cybersecurity administration [earlier this year] implemented a set of new regulations on the governance of the ‘online information content ecosystem’ that encourage ‘positive’ content while barring material deemed ‘negative’ or illegal.” [Lily Kuo, The Guardian]

- San Antonio council’s anti-hate-speech resolution had a lot of ill-advised content but managed to stop short of overstepping the First Amendment itself [Taylor Millard, Hot Air]

- We reported on SEC gag orders last year (more: Robert McNamara) and now the New Civil Liberties Alliance is in court to challenge another one [Peggy Little, NCLA on SEC v. Romeril]

- Once censorship to regulate “online harms” gets its foothold the topics of its meddlesome ambition will expand [Charles Hymas on demands in Britain that “body shaming” in social media be subject to legal sanction]

Posts Tagged ‘Securities and Exchange Commission’

COVID-19 pandemic roundup

- “However peaceable we might be in our intentions, our assembling is a physical threat. Our judgments about liberty, I think, need to reflect that.” [Eugene Volokh on freedom of assembly during an epidemic] Suits against quarantine seldom prevail [Chris Dolmetsch and Malathi Nayak, Bloomberg/Claims Journal] Quarantine and public health measures set important precedents in overcoming judges’ suspicion of delegations of power [Keith Whittington]

- If the federal government decided it wanted to block movement between different states to combat virus transmission, where would it get the legal authority, and what means could it lawfully use? [Gene Healy, Cato] The constitutional background on freedom to travel, as well as search and seizure, during an epidemic [Volokh]

- “The common law also appears not to be a good alternative. One can imagine the litigation nightmare if everyone who got the virus attempted to identify and sue some defendant for damages.” [Tim Brennan, Truth on the Market]

- Cracking down on putatively deceptive accounting practices, SEC penalized “‘bill-and-hold’ transaction orders in which a product is not immediately delivered to its customer.” And that was terrible news for anyone in the business of trying to build public health stockpiles — of vaccines, equipment, PPE — that might be needed in a contagious-disease emergency [John Berlau, CEI] Better than compulsory purchase orders: “Using Purchase Guarantees and Targeted Deregulation to Boost Production of Essential Medical Equipment” [Caleb Watney and Alec Stapp, Mercatus Center]

- Flashpoints include drive-in services, curfews, ID and quarantine of churchgoers: “Religious Freedom Clashes With Public Health Enforcers” [Elizabeth Nolan Brown]

- “FDA Denaturing Rules Are Toxic for Small Distillers” [Jacob Grier]

Federal charges belong before federal courts

“How many unconstitutional administrative trials must one endure before getting the chance to argue your case in an Article III court? According to the U.S. Securities and Exchange Commission, the answer is at least two.” [Russell Ryan, Ashley Parrish, Ilya Shapiro, and William Yeatman on Cato amicus brief in Lucia v. SEC, a case that has already made a trip to the Supreme Court]

Banking and finance roundup

- Supreme Court poised to strike down structure of Consumer Financial Protection Bureau (CFPB) as unconstitutional [Ilya Shapiro, National Review]

- No love lost between Elizabeth Warren’s, Barack Obama’s teams when consumer finance regulation was on the table [Alex Thompson, Politico]

- Cato Daily Podcasts on two topics with Diego Zuluaga and Caleb Brown: Congress is considering a ban on cashless stores, and Bernie Sanders wants to create a public credit scoring system;

- And speaking of the Vermont senator: “The Economic Consequences of Sen. Sanders’ Stock Confiscation Plan” [Ryan Bourne, Cato]

- State Street hearing before Boston federal judge lays bare politics and accounting issues of one large securities class action settlement [Daniel Fisher/Legal Newsline and more, Law360 also via Fisher]

- SEC rules on “accredited investors” are an attempt “to protect us from ourselves. Yet there are no such rules for betting in Las Vegas.” [David Henderson]

Banking and finance roundup

- Progressive sentiment vs. actual progress: Philadelphia bans cashless stores [Jeffrey Miron; related, Billy Binion, Reason (council member thinks city should legislate against “elitism”), Joe Setyon, Reason (NYC)] Meanwhile, heading in the opposite direction: “California bill would require businesses to offer e-receipts” [Don Thompson, Associated Press]

- “Overhaul CRA? Why Not Eliminate It?” [Diego Zuluaga, American Banker; video of panel on CRA at Federalist Society National Lawyers Convention with Bert Ely, Deepak Gupta, Keith Noreika, and Jesse Van Tol, moderated by Hon. Joan Larsen]

- SEC should see its role as fostering, not just reining in, risk taking [Cato audio with Commissioner Hester Peirce; more from Peirce, Cato Journal]

- Your taxes pay for bad mortgage loans [Hans Bader]

- “With Emulex Corp., Supreme Court Could Raise Bar for ‘Merger Tax’ Securities Suits” [Stephen Bainbridge, WLF; Emulex Corp. v. Varjabedian]

- In car insurance, credit scores “effectively predict risk of claims within racial and ethnic groups” and banning their use would likely “result in insurers finding other, less good and possibly discriminatory methods of distinguishing high from low risks” [Luke Froeb, Managerial Econ via Alex Tabarrok]

March 6 roundup

- A longtime progressive objects to the diversity pledge (applying to personal and professional lives alike) soon to be expected of Ontario lawyers and paralegals as a condition of their licenses [Murray Klippenstein with Bruce Pardy, Quillette]

- More on Cato’s First Amendment challenge to SEC gag-order settlements [Cato Daily Podcast with Clark Neily, Robert McNamara, and Caleb Brown]

- “Federal judge sanctions lead lawyer in Roundup trial for opening statement ‘misconduct'” [Debra Cassens Weiss, ABA Journal]

- Unanimous high court (Sotomayor concurring in judgment) rules Ninth Circuit may not count Judge Stephen Reinhardt’s vote in decisions issued after his decease: “Federal Judges Are Appointed for Life, Not for Eternity” [Eugene Volokh]

- Copyright law firm has “a pattern of making aggressive and, in many cases, unsupportable demands” for payment [Paul Levy, CL&P]

- “Genealogists shouldn’t have to become technophobes,” yet to spit in a cup is now to enter oneself and one’s relatives intoto a genetic panopticon for the benefit of law enforcement [Matthew Feeney, Real Clear Policy]

Cato challenges SEC gag-order settlements

When the Securities and Exchange Commission settles with defendants, it extracts gag orders forbidding them forever after from making or causing to be made “any public statement denying, directly or indirectly, any allegation in the complaint.” We noted that fact briefly in yesterday’s roundup adding the question: Is it constitutional for the government to do that?

It isn’t according to the Cato Institute, which wants to publish as a book a businessman’s personal memoir telling his side of the story about his legal battles with the SEC, but cannot do so given that he consented to a settlement containing the gag order. Cato, represented by the Institute for Justice, has now filed suit seeking a court determination that the government cannot use gag orders in settlements to silence those it accuses of wrongdoing. [Clark Neily, Cato at Liberty]

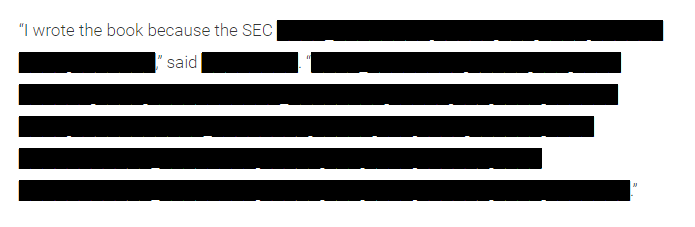

IJ’s press release about the case has fun with redaction:

January 9 roundup

- Maker of Steinway pianos threatens legal action against owners who advertise existing instruments for sale as used Steinways if they contain other-than-factory replacement parts [Park Avenue Pianos]

- When the Securities and Exchange Commission settles with defendants, it extracts gag orders forbidding them to talk about the experience. Is it constitutional for the government to do that? [Peggy Little, New Civil Liberties Alliance/WSJ] Update: Cato is suing about this on behalf of former businessman who wants to write book about his experience in court against the SEC [Clark Neily]

- Judge preliminarily enjoins New York City ordinance requiring home-sharing platforms like AirBnB to turn over to authorities “breathtaking” volume of data about users [SDNY Blog]

- U.S. Chamber’s top ten bad lawsuits of 2018 [Faces of Lawsuit Abuse] “The Most Important Class Action Decisions of 2018 and a Quick Look at What’s to Come” [R. Locke Beatty & Laura Lange, McGuire Woods]

- “Small aircraft engines are much less reliable than automobile engines. Why? Well, they all must be FAA certified, and it’s not worth the cost to certify, say, a new model of spark plug.” [John Cochrane, who gives HIPAA and military examples too]

- “Why logos and art are sometimes blurred on reality TV shows” [Andy Dehnart, Reality Blurred, 2017]

Elizabeth Warren’s proposals on business organization

Schemes like a government mandate of worker representation on corporate boards (an element of German “co-determination”) are not new, and scholars have studied their track record in Europe for years. In particular, they tend not to provide robust incentives for risk-taking and dynamism; that’s aside from their interference with the contractual liberty of all parties to adopt alternative governance methods agreed to by all parties. I talk with Cato’s Caleb Brown about that and Massachusetts Senator Elizabeth Warren’s other ideas for revamping how large companies are run. Earlier here and here.

Banking and finance roundup

- “State-run retirement plans are the wrong way to protect the poor” [Andrew G. Biggs, AEI]

- Fifth Circuit panel: Federal Housing Finance Agency (FHFA) “is unconstitutionally structured and violates the separation of powers” [Jonathan Adler] Unconstitutional structure afflicts Consumer Finance Protection Bureau too [Ilya Shapiro on Cato amicus brief in Fifth Circuit case of CFPB v. All American Check Cashing, earlier here, etc.]

- Study: financial advisers in Canada who are not subject to fiduciary duty have personal investments similar to their clients [Peter Van Doren]

- Regulation can have a lulling effect. Might it even breed financial illiteracy? [Diego Zuluaga, Cato]

- “As I predicted, the ratchet effect is going to save Dodd-Frank. Sigh.” [Bainbridge]

- “SEC proposes to limit whistleblower awards” [Francine McKenna, MarketWatch]